But just keep in mind; just because you can utilize a specific kind of loan to pay for an addition, it does not imply it's going to be the best option for you. And we'll break down the benefits and drawbacks of 6 various choices to assist you to identify which path you must decrease. Simply keep in mind that making the incorrect option can increase your monthly payments, limit your borrowing power or both. Here's what you'll learn and whatever that we'll check out: Home additions, tasks that increase the total living area of your home either horizontally or vertically, can can be found in all shapes, sizes, spending plans, and functions, which will all most likely play an aspect when deciding the financing alternative that's best fit to your project.According to Home, Consultant, the average expense to develop an addition or including a space to your house is $46,343, with most projects being available in between $20,864 and $72,244 depending upon the scope and requirements.

These are extra rooms and areas contributed to the home, which broaden the square footage. Depending on the scale of work, these also take the longest to complete and generally cost the a lot of. This kind of task likewise includes the similarity sunroom and garage additions. Instead of creating a totally new space, micro additions, otherwise known as bump-out additions, extend from existing rooms. Therefore, they provide an easier and more affordable option for those who do not seem like they need as much extra area. What jobs can i get with a finance degree. When building outwards isn't readily available to you, a second story addition could be the very best option for producing more area.

It's likewise worth keeping in mind that developing is typically rather less expensive than adding on - How many years can you finance a boat. In most cases, building vertically can offer the ideal option for extra bedrooms or restrooms or perhaps a master suite. Your household might have outgrown your house, however you do not wish to move. Perhaps you have been appealing yourself that dream kitchen area for a while now. Maybe you wish to produce the space that everyone in your family requires as your kids turn into young people. Everyone has a different inspiration for producing an addition to their home, but what are the main advantages of building onto your existing property?One of the most typical inspirations for a home addition is simply to delight in additional home that can be tailored to personal needs.

Not only can a home addition be less expensive and easier than moving, however perhaps you fret that finding another property in your preferred area may be challenging given the real estate stock lack that we discover ourselves in the midst of right now. Including additional area to your existing home saves the disruption of rooting out from friends, next-door neighbors, schools, and the amenities you currently enjoy in your current place. While it is not always ensured, usually an addition to your house is going to be a here monetary investment that increases the general worth of the property. Even if you are not planning to move for a considerable amount of time, a remarkable addition will include curb appeal if you do wish to sell in the future.

Take the time to understand the differences in between these six different ways to finance your addition and thoroughly consider which can help you to borrow all of the cash you require with the most affordable regular monthly payments.Reno, Fi Loans are a new type of house restoration loan that provide the best method to fund a house addition by extending your borrowing power even further. Unlike traditional home equity loans, Reno, Fi Loans aspect in what your house will be worth after the work has actually been completed, as a result, increasing your loaning power by 11x as you can see in the example below: This makes a Reno, Fi Loan a fantastic choice for recent property owners who haven't developed enough tappable equity to get a home equity loan or home equity line of credit however are nevertheless desperate to start on the addition.

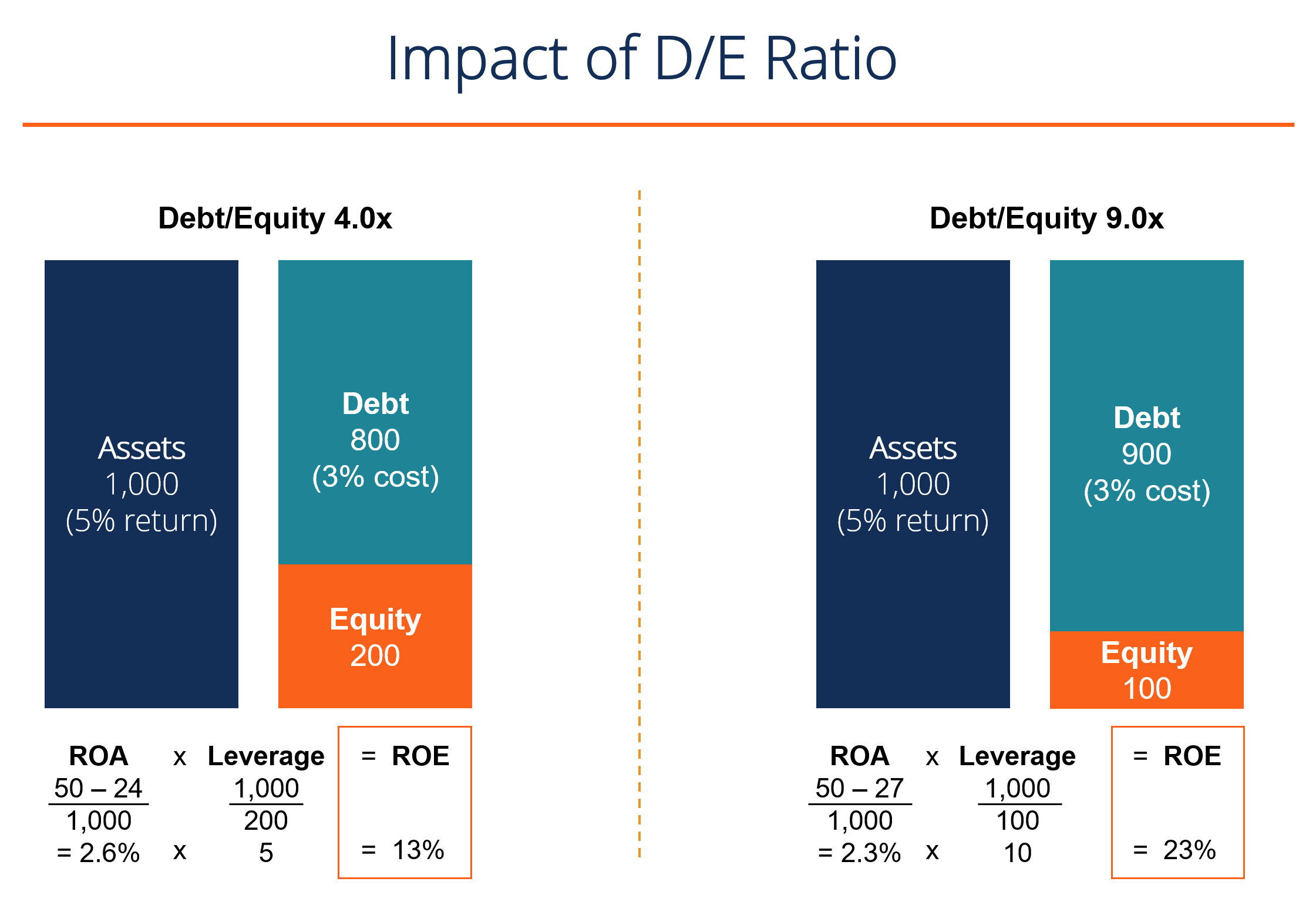

All About Trade Credit May Be Used To Finance A Major Part Of A Firm's Working Capital When

How much more might you anticipate to borrow with a Reno, Fi Loan?Let's say your house deserves $500,000 today and you currently have a home mortgage of $350,000. With a typical house equity loan, you may anticipate to obtain around $50,000. However the prepared addition to your house will take the value after timeshare floating week explanation the project is finished as much as $750,000. A Reno, Fi Loan, in this wesley mcdowell example, could let you borrow up to $350,000. That's a big boost in your borrowing power. With terms as much as 20 years and your loan based upon the after renovation value, a Reno, Fi Loan permits you to benefit from lower market rates compared to the greater rate of interest of a number of the alternatives.

This is a second mortgage that's perfectly matched to this kind of job, which means you can keep your low rates and do not have to begin the clock once again on your home mortgage. Put merely, for the majority of property owners, a Reno, Fi Loan offers the most money and least expensive regular monthly payment and unlike a few of the alternatives, there aren't any examinations, specialist involvement, or draws to contend with. Here's how these loans stack up against some of the other alternatives that you're probably thinking about: Remodelling House Equity Loan, Single-Close Building To Long-term Loan (CTP) Fannie Mae Home, Design Loan, FHA 203k (Full) Two-Close Construction To Irreversible Loan (CTP) Is this a mortgage?Yes, Yes, Yes, Yes, Yes1st or 2nd home loan? 2nd1st1st1st1st, Need refinance of existing mortgage?No, Yes, Yes, Yes, Yes, Typical Rate Of Interest, Market, Above Market, Above Market, Above Market, Above Market, Loan Limit (Restoration Expense + Home Loan)$ 500,000 Jumbos enabled, Conforming only, Adhering only, Jumbos allowed, Loan Term (max) 20 years30 years30 years30 years30 years, Credit report Required660 +700 +620 +580 +580+ Loan to Worth, Up to 95% Up to 95% Approximately 95% Up to 96.

The Reno, Fi team is waiting to help you much better comprehend how Reno, Fi Loans work and the jobs they are best fit for. Have a concern - Chat, Email, Call now ... A house equity loan or credit line (HELOC) permits you to take advantage of any equity you have actually already generated through settling your home mortgage to launch a lump sum that can then be used to spend for your addition. You can rapidly exercise the amount of equity that's in your home by merely subtracting what you owe on your home mortgage from the existing worth of your residential or commercial property.

You need to understand though that a common home equity loan will just enable you to borrow as much as 80% of the house's worth, implying that if your property is worth $500k right now and your impressive home loan balance is $350k, the most you'll be able to obtain is $50k. However for lots of property owners, there's one substantial issue with these loans, and the biggest drawback is that if you have not owned your house for long, chances are that you may not have actually collected much equity. Simply take a look at the length of time it can require to build up $100k equity: Financing a house addition can be extremely expensive and frequently needs a big injection of money and the truth is that those who have only recently purchased their property and who haven't yet got sufficient tappable equity, this isn't going to be a choice.